Rishi Sunak Expected to Extend Covid Recovery Loan Scheme

The Chancellor is expected to announce an extension to the Government's Covid recovery loan scheme, which was set to end on December 31st, in his budget speech next week.

The Chancellor is expected to announce an extension to the Government's Covid recovery loan scheme, which was set to end on December 31st, in his budget speech next week.

Leaked documents reveal that the Treasury is concerned about the economic costs of moving towards a zero-carbon economy, including companies being pushed by green initiatives to move production abroad.

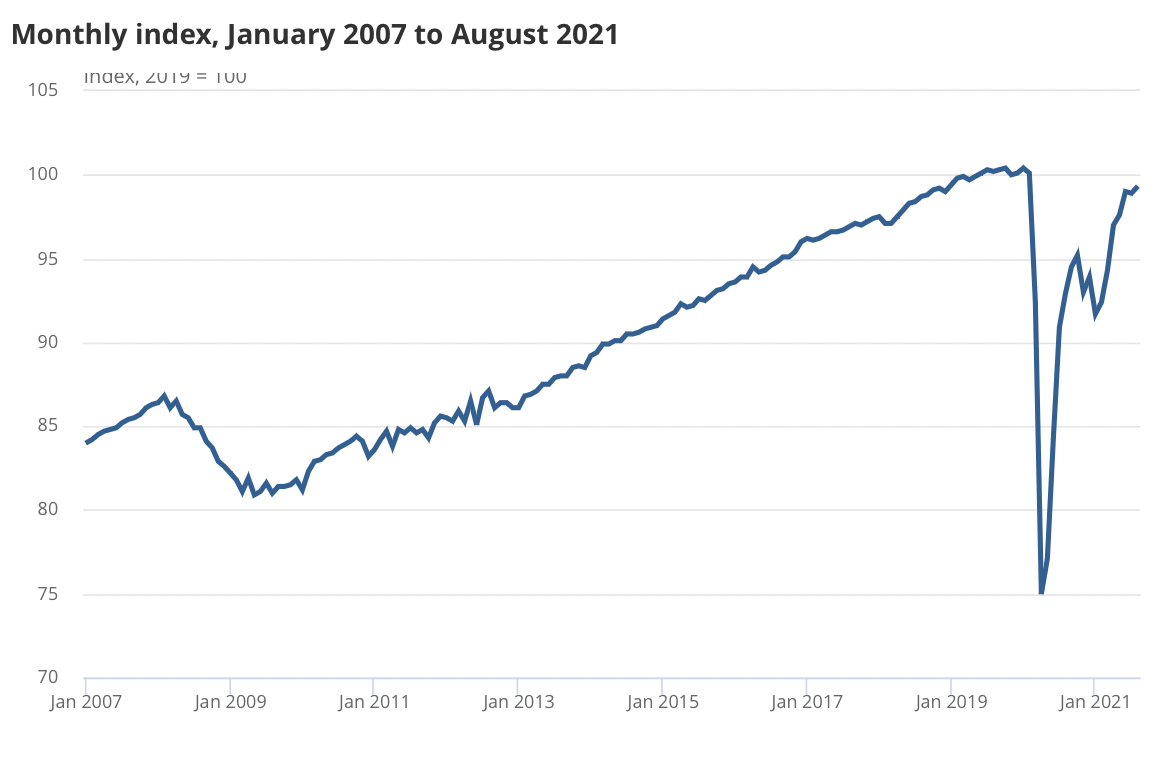

The latest ONS data shows that GDP growth was lower than expected in August, and still lower than pre-lockdown levels. Figures for July have also been revised downwards in a blow to the Treasury.

Government borrowing last month was the second highest figure for August on record and came in £5 billion higher than was expected.

A surge in bankruptcies is expected in the hospitality sector as business support runs dry, with a partner at an insolvency firm saying "we have yet to see the full extent" of lockdown's financial hit on resturants.

More than £2 billion has been splashed by the Government on PPE that was so useless it could not be used in the NHS – five times higher than initial official estimates.

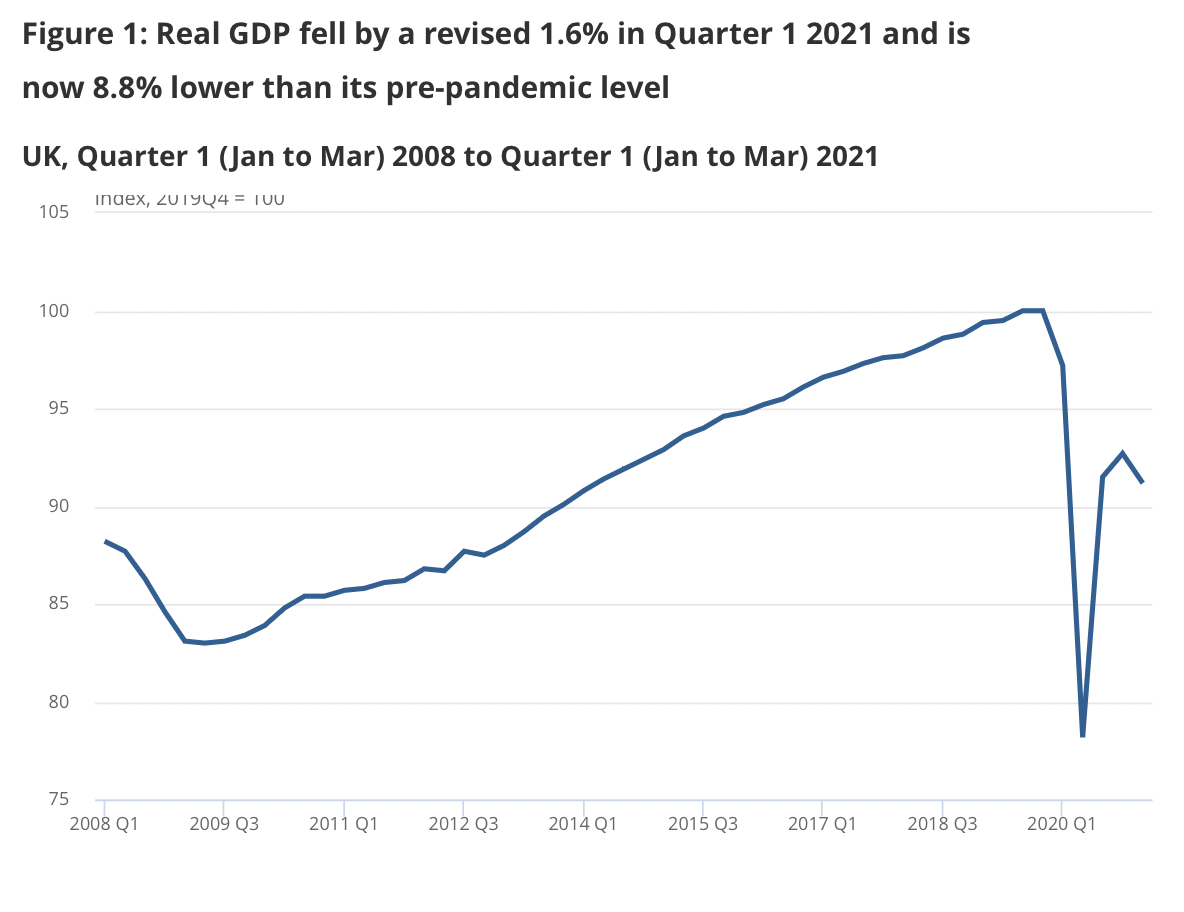

The economy shrank by 1.6% in the first quarter, more than was previously thought, as ONS data shows that the real GDP level is now 8.8% lower than its pre-lockdown level.

With the Government having borrowed another £24 billion in May and the national debt standing at £2.2 trillion, a former Chancellor has warned there is a "big risk" of inflation spiralling out of control.

The Government is considering extending lockdown by a month rather than by two weeks so as to give businesses "certainty" that "Freedom Day" won't be delayed again.

Researchers in the U.S. have projected that productivity losses caused by school closures during lockdowns will lead to a 3.6% decrease in GDP and a 3.5% decrease in hourly wages by 2050.