Liz Truss’s efforts to divert the blame for her downfall from her mini-Budget to the Bank of England has received support from some unlikely quarters in the past few days.

If you want a refresher on the role of the Bank of England in creating the market turmoil that followed the min-Budget, this piece by Jon Moynihan, published yesterday in CapX, is well worth a read. It includes a crash course in Liability-Driven Investment funds, which were at the root of the precipitous rise in bond yields that ultimately did for Truss.

So, who are Liz’s unlikely allies? Robert Peston, for one. On Sunday, he tweeted: “Liz Truss is completely right about one thing. It is astonishing that the Bank of England, the Pension Regulator and HM Treasury were so wrong footed by pension funds’ fire sale of government bonds and other assets as a result of their massive over-use of LDI hedging…”

Then, there’s Patrick Hosking, the Economics Editor of the Times. He has written a piece this morning in which, while he doesn’t entirely exculpate Truss, nevertheless accepts that she’s essentially right about the role of LDIs in her downfall. Here’s an extract:

Economic historians no doubt will argue about that, but no one would dispute that the crash of government bond prices and the surge in their yields, which move inversely to prices, did for her personally. The ensuing slump in the pound and the jump in new mortgage rates were seen by her own backbenchers as a damning verdict.

How much was down to the liability-driven investment “tinderbox”, as she calls it, is harder to say. The House of Lords industry and regulators committee, a cross-party group chaired by Labour’s Lord Hollick, largely sides with her on this narrow point. It says today that while the mini-budget was “the trigger” for the gilts market dive, “we believe that the downward spiral was caused by the presence of leverage in LDI funds”.

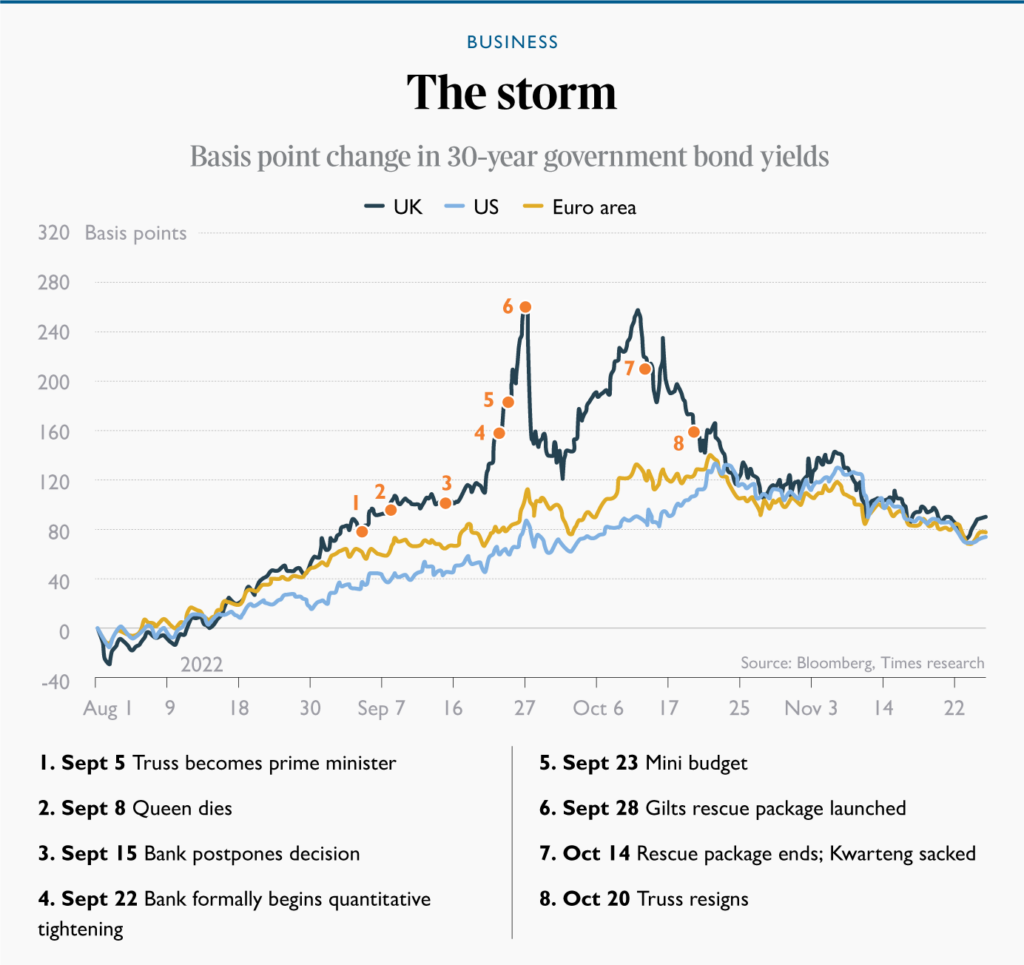

It was a complicated moment in markets and politics. Three big themes were playing out in late September. The first was a significant worsening of inflation and therefore rising interest rate expectations both worldwide and in Britain. The second was the uncertainty of the Truss era and how that might affect the UK’s appeal to international investors. The third was the gradually growing stresses in pension funds’ LDI positions. There was also a fourth element at work — the death of the Queen. This led to a near-paralysis in policymaking for more than a fortnight and persuaded the Bank of England to postpone its monetary decision-making by a week.

Disentangling these forces is nigh-on impossible, but it is important to try, not only to understand Truss’s downfall but also for deciding how Britain should reset policy to minimise the chances of a repeat of the LDI debacle. The chart above sets out the sequence of events. There are several immediate observations.

The first is that the trajectory of UK yields started to diverge from European and American yields pretty much from the moment in late August that it became clear Truss would win the Tory leadership election. Anxious investors started to demand a premium to hold UK government bonds. The second is that yields started to accelerate sharply not from the day of the mini-budget but the day before, when the Bank raised base rate and officially pressed the button on quantitative tightening. It has always insisted that its tightening plans were well telegraphed, but formally announcing that it would start to sell £80 billion of its stockpiled bonds certainly didn’t help.

The third is that, but for the period of mourning, the official monetary tightening would have taken place a week earlier. Arguably, it might have led to a flatter, more gradual slope in rising yields. Might that have made a difference? The liability-driven investment squeeze was mostly down to the rate of change in yields. It was not the rise in yields, but the speed at which they rose that wrong-footed pension funds and left them scrambling to find cash for margin calls quickly enough. That led to more gilt sales and the terrible self-feeding selling spiral that followed.

Truss’s suggestion that she was undermined by a left-leaning economics establishment sounds borderline paranoid. The Treasury and Office for Budget Responsibility were merely reflecting the, yes, orthodox way bond investors think. But she is right to believe the turmoil was enormously amplified by the fatal flaw in liability-driven investment.

It remains to be seen what the Government or the Bank of England or the pensions regulator does about LDIs. But as Peston goes on to say in the same Tweet thread, “This was the most serious regulatory failure since the 2007/8 banking crisis.“

Patrick Hosking’s piece is worth reading in full.

To join in with the discussion please make a donation to The Daily Sceptic.

Profanity and abuse will be removed and may lead to a permanent ban.

Incompetence. Yeah right.

That aside:

If they’re so incompetent, why are we expecting them to solve the problem of underfunded pensions with regulation?

The problem with pensions is that pensions were invented at a time when the retirement age was basically the same as life expectancy, and the population pyramid had lots of working people at the bottom and very few pensioners at the top.

`And now we have people living 20 years past retirement and a population pyramid with tonnes of pensioners and not enough working people to sustain them.

The problem isn’t a B of E regulation problem it’s an ostrich problem. When it comes to pensions our society, indulged by our politicians has been burying its head in the sand for decades.

Everyone knew full well this was coming but as a society we’re completely paralysed on this issue.

When private sector defined benefit pension schemes were launched the employer had much more flexibility. The pensionable age could be held down so the assets would meet the obligations, contributions holidays could be used and no accrual or catch-up payments had to be made. Regulations and therefore the operating costs of the schemes were far far lower – nowerdays even closed schemes cost a lot to keep in place.

HMG / politicians interferred without much understanding and very many good businesses have gone bust as a result. Note always that Parliamentarians, their staff and the civil service were never affected by all this.

I have no doubt that successive givernments have made things worse with their regulations, as they always do.

Not helped by Gordon Brown raiding private pensions so he could continue his spending incontinence.

Also not helped by Brown giving companies a pensions contribution holiday, because companies “were never going to need so much money in their pension schemes”.

Is it any wonder he sold the country’s gold at the bottom of the market?

.

Not helped by the Pensions Regulator pushing company pensions into government bonds for over a decade, when the financial crash left them even further underfunded, rather than letting them use equities to close the funding gap.

Just a coincidence that this “incompetence” came on suddenly to coincide with a new PM who had selected a Cabinet some of whom threatened to behave like conservatives, with a budget that departed from the current accepted norms.

When ‘mistakes’ all favour one outcome over any another, they are in fact ‘decisions’…

‘Coincidence’ and ‘incompetence’ becomingly increasingly popular I see. As they have done for hundreds of years, with the same outcomes, from the same people.

Another coup to insert a more favoured son.

The BoE was not just incompetent. They are complicit as well. What the BoE did not see coming as fast as it was – was the Pension LDI Derivatives. Where the complicit comes in is that these LDIs are all OTC (Over the Counter) and thus un-regulated.

How can the funding mechanisms for UK pension funds be OTC and have an exponential 3rd Party counter-risk?

BoE (and their independent shareholders) are driving the monetary policy (and it seems the fiscal policy) to a point-collapse at some juncture in time (of their choosing), so they can bring in CBDCs and UBI without resistance. The Pension LDI collapse was not convenient to their timing.

The BoE (and their Independent shareholders – who are the same shareholder over most international CBs i’d wager?) must, repeat must maintain control with the only solution when the resonance of multiple unknown Derivatives collapse at the same time.

The best game in town is to be the House, set the table rules and insist on being the monopoly solution (getting rich from chaos and THIER rules).

When it fails and it will fail shortly, we have to ensure the current people behind the scenes now are not selected to run a “new” and “improved” CBDC financial system. They have had multiple chances in the past and blown them all. We have to stop paying the price.

Oh, the regulator failed again……

As Beatty didn’t quite say at the Battle of Jutland:

‘There seems to be something wrong with our bloody regulators today!’

The detail may be of interest to future generations but all we need to know, and many have thought it since it happened, was that the various blobs contrived to get rid of Truss.

That is the long and short of it. Outrageous behavious by the blobs which they were conbfident of because they are used to determining who can be UK PM.

Or some might say (as at least one observer on GBN yesterday said) that the BoE won, and got rid of someone they didn’t like.

When she emerged as our new PM, I thought – bleedin’ ‘ell is that the best we can do?

Clearly it was. Can we have her back please?

When Peston is on the side of ‘Incompetence’ it is an absolute certainty that Incompetence is not the reason for Ms Truss’s ousting.

The post I made on this matter on the 5th

does not therefore stand to be revised and with apologies to those who have already seen this:

Well, there’s no denying Toby’s eternal optimism given that he is falling for cock-up rather than conspiracy. Again.

This story reminds me of the inimitable Mrs Merton and the point in her talk show where she announces – “let’s all have a heated debate.” In other words a cover story has been put out to create yet another diversion. Is something afoot again?

To deny the fact that Liz Truss was deliberately ousted is simply ridiculous and it had nothing to do with the markets, that is complete BS.

Liz Truss, on being selected by the Conservative membership and immediately on taking office as PM acted to bring some economic stability to the country. Possibly her proposals would have helped but what is fundamentally assured is that her measures were completely contrary to the requirements of the WEFfers and the Davos Deviants. She was definitely not with the script and so had to go. Whatever shenanigans took place orders went out firstly to install Chunt – a man despised by his fellow MP’s, and reviled by the party membership – and once he had his feet under the table Truss was indeed to be forced “into a dark room with a glass of whisky and a revolver.”

In a pantomime version of an election all the ‘aspiring’ candidates somehow managed to fall by the wayside until only Fishy and Bozo were left – do me a bloody favour! Bozo of course graciously conceded and the Davos plant, still politically wet behind the ears, was installed. Very much in keeping with all the rest of the lies and deceit now infecting the country like, oh I don’t know – a virus.

There will need to be a much stronger body of evidence to persuade me that Liz Truss wasn’t ousted in the most blatant and grotesque example of a coup that I have ever seen in this country. To suggest she was removed as a result of ‘the markets’ is beyond farcical.

“It’s not always about what they say it’s about.”

Nailed it. Cognitive dissonance obviously doesn’t apply as long as you mention ‘incompetence’, ‘markets’ and as much gobbledygook as possible.

Most on here getting it though – apart from Tobes of course.

Truss was half unlucky – half daft

The UK doesn’t set its interest rates anymore

It follows the USA

We are reduced to the status of a poor European country

Crippled by social security costs

Funding day to day expenses by money printing

International lenders won’t lend to us as we are such a basket case

So when the USA raised it rates we had to also

or the £ would have collapsed further

This was compounded by the Pension Fund over borrowing

She was daft thinking she could spaff £65,000,000,000 on energy relief

The Tories are an irreconcilable blob

From Conservatives, Liberal Democrats + Progressives

But they have no balls (are so average)

So they stay secure in the Tory nest

Its not a good prognosis

Toby, it’s nothing to do with ineptitude, it was entirely purposeful on the BoE’s part. How can you believe that the BoE would be inept?!! And you’ll put up with it or trust them to run things?

From an earlier Moynihan piece in the Critic

One part of, but not all of, the case against the Bank has been cogently made by Narayana Kocherlakota, a well-respected economist and former president of the Federal Reserve Bank of Minneapolis, in a Washington Post piece entitled “Markets didn’t oust Truss — the Bank of England did”.

The question might be asked – Why? Could be the green finance rentier class did not like Truss freeing up fracking, which would have undermined their wind and solar investments. Was Mark Carney Bailey’s former boss? Have a look at Brookfield Asset Management, chaired by Mr Carney. $68bn in renewables https://www.telegraph.co.uk/business/2022/12/26/mark-carneys-investment-company-closing-major-octopus-energy/ And the Glasgow Financial Alliance For Net Zero.

Interesting. So the bottom line (for Liz Truss) was a bunch of economically clueless MPs panicking when the ‘markets’ hiccupped. Fundamentally, lowering tax rates was the correct move to stimulate the economy, which is the govt’s priority, not the markets.

It just strikes me that we’ve allowed the relationship between the economy and the markets to be reversed, i.e. let the markets control the economy. My gut feeling is that was a serious mistake, and the UK govt needs to reassert economic control.